Understanding how your loan payments are structured over time

Amortization means a variety of different things i.e., it can mean distributing any expense or cost across multiple periods instead of recognizing it all at once, it can also mean spreading the cost of an intangible asset (like a patent or trademark) over its useful life, or as in most cases means gradually paying off a debt (like a mortgage or car loan) through regular payments over time. For this article, we shall focus on loan amortization.

If you’ve ever taken out a loan, you’ve already experienced amortization, whether you knew the term or not. It’s one of those financial concepts that quietly shape how much you pay over time, yet it’s rarely explained in an intuitive way. At its simplest, loan amortization is the process of paying off a debt through regular, fixed payments over a set period. But what makes it interesting and important is how each of those payments is divided.

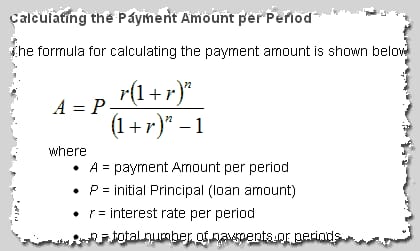

See, every time you make a loan payment, you’re not just “paying back the loan.” You’re covering two things at once: the interest charged by the lender and a portion of the original amount you borrowed, known as the principal. Early in the life of the loan, most of your payment goes toward interest, but as time goes on, that balance shifts, and more of your payment starts reducing the principal. This shift isn’t arbitrary, and it’s not a trick. It’s simply the result of how interest is calculated.

In most scenarios, interest is based on the remaining balance of your loan (reducing-balance method). At the beginning, that balance is at its highest, so the interest portion of your payment is also high. Even if your monthly payment stays the same (Fixed interest method), a larger share of it goes toward interest in the early stages. As you continue making payments and the balance gradually decreases, the interest charged each period becomes smaller. That leaves more of your fixed payment available to reduce the principal.

The result is a kind of financial progression. At the start, your payments feel like they’re barely making a dent in the loan itself, but somewhere in the middle, things begin to balance out. Toward the end, most of what you pay goes directly toward eliminating the remaining balance. The payment amount never changes, but its impact does.

To make this concrete, imagine borrowing a small amount, say $1,000, at a fixed annual interest rate, to be repaid over a year. Your monthly payment might feel straightforward and predictable. But under the surface, the first payment is doing very different work from the last one. In the beginning, a noticeable portion is absorbed by interest. Near the end, almost the entire payment goes toward finishing off the loan. The structure is consistent, but the composition evolves.

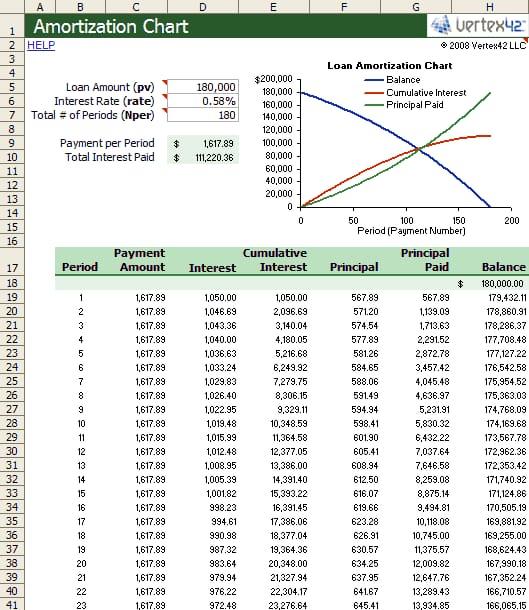

This is exactly what an amortization schedule captures. It’s a detailed table that shows each payment over time, breaking it down into interest and principal while tracking the remaining balance. Seeing it laid out this way often changes how people think about borrowing. What seemed like a flat, repetitive series of payments becomes a dynamic process with a clear direction.

Understanding this pattern also explains why timing matters so much when it comes to saving money on a loan. Because interest is highest when the balance is highest, reducing the principal earlier has an outsized effect. Even small extra payments made in the early stages can significantly reduce the total interest you’ll pay. The same extra payment made near the end of the loan has a much smaller impact, simply because there’s less balance left to generate interest.

This is one of the most practical insights amortization offers. It’s not just about understanding how loans work, it’s about knowing how to use that structure to your advantage. Paying a little more, a little sooner, can shorten the life of the loan and lower its overall cost.

There are, of course, variations on the basic idea. Some loans are not fully amortized, meaning they don’t completely pay off by the end of the term and may require a large final payment. Others allow for changing interest rates, which can alter the payment structure over time. In more unusual cases, a loan can even enter negative amortization, where payments are too small to cover the interest, causing the balance to grow instead of shrink. But the core principle remains the same: interest depends on what you still owe. This is also why it is very important to understand interest rates on the loan. See interest rate is not just a certain percentage; it can be fixed or changing, high or low and so many other variables.

One of the most persistent misconceptions about amortization is the idea that lenders deliberately “front-load” interest to maximize their profit. In reality, the pattern emerges naturally from the mathematics of compound interest. The lender isn’t rearranging the payments to disadvantage you; the structure is simply a reflection of the declining balance over time.

Once you understand that, the whole system becomes far more transparent. A loan stops being a black box and starts to look like a predictable sequence of cause and effect. Higher balances generate more interest. Lower balances generate less. Fixed payments gradually shift from servicing the cost of borrowing to eliminating the debt itself.

And that clarity is useful. Whether you’re taking out a personal loan, financing a purchase, or considering a mortgage, knowing how amortization works gives you a clearer picture of what you’re actually paying for and how you might reduce that cost.

In the end, amortization isn’t just a technical detail buried in loan documents. It’s the rhythm of how debt is repaid. Once you see the pattern, it becomes much easier to make decisions that work in your favor.

Use our Loan calculator to see how your loan payments breakdown over time.